Paris

13 addresses

Our experts will guide you in your choice of domicile.

Our experts will guide you in your choice of domicile.

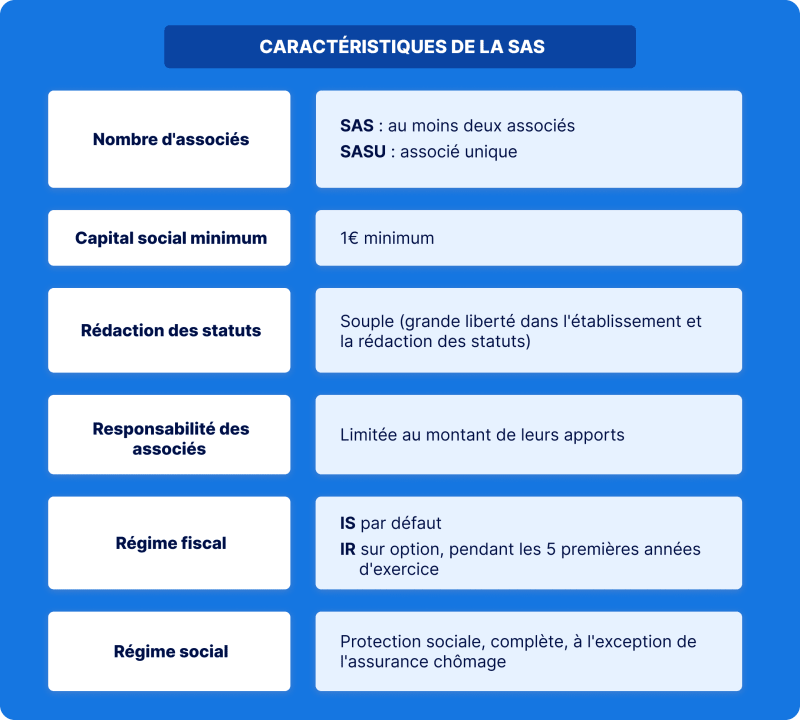

The SAS is a particularly popular legal form, thanks to its great operational flexibility. Normally made up of at least 2 partners, it can also be created by a single partner, in the form of a SASU.

The SAS is a legal form with many features. This legal form, which must have at least two partners, can be created with a minimum share capital of just €1 .

Particularly appreciated for its great flexibility, the SAS allows you to draw up your own articles of association, letting you organize your company's operating rules as you see fit.

What's more, the liability of SAS shareholders is limited to the amount of their capital contributions. In the event of debt, each partner is liable only to the extent of his or her share in the company's capital.

With SASU, you can go it alone in entrepreneurship, while enjoying all the advantages of SAS. The SASU is simply the single-member form of the SAS, meaning that it has only one shareholder.

In principle, a SASU (société par actions simplifiée unipersonnelle) follows the same rules as an SAS. They therefore have many points in common:

But what if the sole shareholder subsequently wishes to add new partners? It is possible to transform a SASU into a SAS by opening up the company's capital, if this has been provided for in the articles of association. On the other hand, if no such provision has been made in the Articles of Association, a modification of the Articles of Association will be necessary.

This change can take place in two different ways:

The distinctive feature of the SAS statute is its great operational flexibility. In fact, legislation does little to regulate the operation of an SAS, leaving the partners a great deal of freedom in drafting the company's Articles of Association. When drafting the Articles of Association, the partners are free to set the rules governing the organization and operation of the company:

SAS status offers many advantages:

Even though the SAS has many advantages, you should not forget to consider its disadvantages when choosing your legal status:

Drafting the articles of association of a simplified joint stock company (SAS) is a mandatory step before creating your company. Even if the partners are free to draw up their own articles of association, they must not forget to include certain mandatory details.

Associates benefit from a high degree of flexibility in drafting their articles of association. They can choose how the company is to be managed, how the Chairman is to be appointed and dismissed, and how decisions are to be taken by the partners. This gives them considerable flexibility in the organization and operation of the company.

This freedom can be a double-edged sword since the drafting of bylaws requires the utmost rigor, as the slightest error can lead to blockages in future decision-making .

It is therefore advisable to enlist the help of a legal professional to draw up the articles of association for your SAS.

Even if the wording of the articles of association is free, certain information must be included in them, in particular :

In addition, the Articles of Association must be signed by all SAS partners.

To set up an SAS, a number of formalities must be complied with before final registration. Here are the main stages:

Once your registration is complete, you will be issued with a number ofidentification documents:

Finally, to domicile your SAS, you can use the services of a domiciliation company like SeDomicilier. When you choose our services, you benefit from a prestigious address for your company, and all procedures are 100% online!

The SAS is fiscally advantageous, allowing you to choose between income tax (IR) or corporation tax (IS). What's more, associates can choose to be remunerated in the form of dividends.

In principle, profits generated by an SAS are subject tocorporation tax (IS). However, when you set up your company, you can opt forincome tax (IR), for a maximum period of 5 years, if several conditions are met:

You can also appoint an external auditor to ensure your company's accounting transparency.

SAS shareholders may receive remuneration in the form of dividends, which are not subject to social security contributions.

These dividends are considered as income from movable capital and are subject to the 30% flat-rate withholding tax (PFU ) (12.8% income tax and 17.2% social security contributions).

They can also choose to be taxed according to the progressive income tax scale, with rates ranging from 0 to 45%.

In an SAS, the Chairman is considered as an "assimilé-salarié", which means that he or she is affiliated to the general social security system. He or she benefits from full social protection, similar to that of conventional employees (sickness-maternity insurance, family allowances, work accident insurance, basic pension insurance, supplementary pension insurance and provident insurance), with the exception of unemployment insurance.

In the absence of remuneration, no social security contributions are due.

In addition, dividends received by the Chairman of an SAS are not considered as remuneration, and are therefore not subject to social security contributions. This means that if you choose to be remunerated solely in the form of dividends, you pay no social security contributions. On the other hand, you do not benefit from any social security protection.

The SAS is a flexible legal form, appreciated by entrepreneurs who wish to define their own operating and organizational rules. Before choosing this status, it is essential to define your project needs and fully understand the advantages and disadvantages of the SAS.