La cotisation foncière des entreprises (CFE) est un impôt local dû par toutes les entreprises exerçant une activité professionnelle non-salariée au 1er janvier de l'année d'imposition. Le montant de cet impôt peut varier chaque année et s'appuie sur la valeur locative des biens utilisés par l'entreprise pour exercer son activité professionnelle. Pour tout savoir sur le calcul de la CFE, lisez attentivement notre article !

Le calcul de la CFE diffère selon que l'entreprise dispose ou non d'un local (ou terrain) pour l'exercice de son activité ;

Lorsque l'entreprise dispose d'un local pour exercer son activité, la CFE est calculée en fonction de la valeur locative des biens immobiliers soumis à la taxe foncière et utilisés par l'entreprise pour son activité professionnelle au cours de l'année N-2 ;

En revanche, si l'entrepreneur ne dispose d'aucun local et exerce son activité à domicile (ou chez ses clients), le montant de la CFE est calculé en fonction d'une cotisation minimum, qui dépend du chiffre d'affaires réalisé au cours de l'année N-2 et du taux d'imposition voté dans la commune ;

Un formulaire de déclaration initiale de CFE doit être transmis à l'administration fiscale avant le 1er janvier de l'année suivant la création de l'entreprise.

Domiciliation + company transfer Kbis fast and 100% online

Quelles sont les entreprises concernées par la CFE ?

La cotisation foncière des entreprises (CFE) est un impôt local dû par toutes les entreprises, qu'il s'agisse de sociétés, d'entreprises individuelles (EI) ou encore de micro-entreprises, exerçant en France une activité professionnelle non-salariée.

Le calcul de la CFE diffère selon que l'entreprise dispose ou non d'un local (ou terrain) pour l'exercice de son activité.

Entreprise disposant d'un local

Lorsque l'entreprise dispose d'un local pour exercer son activité, la CFE est calculée en fonction de la valeur locative des biens immobiliers soumis à la taxe foncière et utilisés par l'entreprise pour son activité professionnelle au cours de l'avant-dernière année (année N-2).

La formule de calcul de la CFE est la suivante :

Taux d'imposition de la commune X Valeur locative des locaux professionnels

Exemple : Pour calculer la CFE due au titre de l'année 2025, il convient de prendre en compte le local commercial utilisé en 2023 pour l'exercice de son activité.

Taux d'imposition de la commune

Le montant de la CFE est déterminé en fonction du taux d'imposition de la commune où l'entreprise a son principal établissement. Ce taux est fixé chaque année par une délibération du conseil municipal ou de l’établissement public de coopération intercommunale (EPCI).

Le taux d'imposition varie d'une commune à l'autre : certaines communes ont un taux proche de 35 %, tandis que d'autres se situent autour de 10 %. Pour connaître le taux en vigueur dans votre commune, il est recommandé de vous renseigner auprès de la préfecture.

Contrairement à ce que l'on pourrait imaginer, le taux de CFE à Paris est l'un des plus bas de France (16,52 %). Cela s'explique par la forte concentration d'entreprises dans la capitale. En effet, le taux d'imposition des communes est inversement proportionnel au nombre d'entreprises qui y sont domiciliées.

Si vous désirez bénéficier d'une CFE réduite, il peut être avantageux de choisir Paris comme siège social de votre entreprise. Pour en savoir davantage, nous vous invitons à consulter notre article dédié au lien entre la domiciliation et la CFE.

Bon à savoir : Pour que votre entreprise soit domiciliée à Paris, vous pouvez recourir aux services d'une société de domiciliation, comme SeDomicilier. Il vous suffit de choisir une adresse de prestige parmi celles proposées par la plateforme et de signer votre contrat de domiciliation directement en ligne ! En domiciliant votre entreprise à Paris, vous aurez l'avantage d'une adresse prestigieuse.

Valeur locative des locaux

Les impôts se basent sur la valeur locative cadastrale des locaux professionnels pour calculer la CFE. Ils prennent ainsi en compte la superficie du local, sa catégorie (entrepôt, magasin…) ainsi que sa localisation.

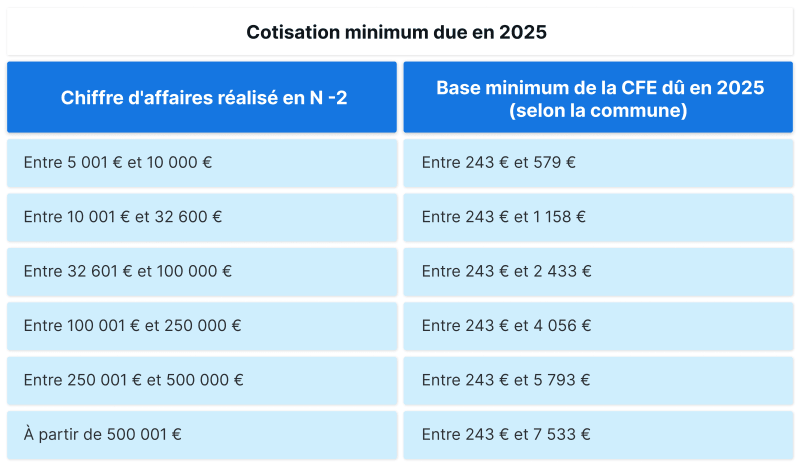

En revanche, si la valeur locative du local est trop faible, l'entreprise doit s'acquitter d'une cotisation minimum, dont le montant est calculé en fonction du chiffre d'affaires réalisé sur une période de 12 mois (au cours de l'année N-2).

Voici le barème applicable en 2025 :

Lorsqu'une entreprise possède plusieurs établissements, la CFE calculée sur une base minimale est due au lieu de l'établissement principal, qui n'est pas nécessairement le siège social de l'entreprise.

Si l'entrepreneur ne dispose d'aucun local et exerce son activité à domicile (ou chez ses clients), il reste quand même redevable de la CFE. Dans ce cas, le montant de la CFE est calculé en fonction d'une cotisation minimum qui dépend :

du chiffre d'affaires réalisé au cours de l'année N-2 ;

du taux d'imposition voté dans la commune.

La formule de calcul de la CFE est la suivante :

Base minimale en fonction du chiffre d’affaires de l’année N-2 x Taux d’imposition de la commune

Voici le barème applicable en 2025 (identique à celui mentionné précédemment) :

Pour chaque tranche de CFE, la base minimale et le taux applicable varient en fonction de la commune dans laquelle l'entreprise est domiciliée. En d'autres termes, deux entreprises ayant le même chiffre d'affaires, mais situées dans des communes différentes, ne paieront pas le même montant de CFE.

Exemple : Vous avez réalisé 35 000 € de chiffre d’affaires en 2023. Vous paierez donc entre 243 € et 2 433 € selon le taux voté dans votre commune.

Il est nécessaire d'informer votre SIE (service des impôts des entreprises) de votre situation. Veillez également à indiquer sur votre déclaration initiale de CFE la surface utilisée pour votre activité.

What are the CFE exemptions?

Certaines entreprises sont exonérées du paiement de la CFE. Voici une liste non exhaustive des cas d'exonération de CFE :

exonération de CFE au démarrage de l'activité ;

exonération de CFE en raison du chiffre d'affaires faible ;

exonération de CFE au titre de l’activité exercée ;

exonération de CFE en raison de la zone d'implantation.

Exemption from CFE at start-up

Les entreprises nouvelles sont automatiquement exonérées de CFE au titre de leur première année d'activité, c’est-à-dire de la date de création jusqu'au 31 décembre de la même année.

Ensuite, elles bénéficient d'une exonération partielle de CFE à hauteur de 50 % au titre de l'année suivant celle de la création.

Exemption from CFE due to low sales

Companies with annual sales of less than €5,000 are exempt from CFE. Sales are calculated over 12 consecutive months.

Exemption from CFE for the activity carried out

Certaines entreprises sont exonérées du paiement de la CFE en raison de l'activité qu'elles exercent. Voici les principales activités concernées :

certains artisans ;

chauffeurs de taxis ou d'ambulances ;

activités de pêche ;

peintres, sculpteurs, graveurs ;

artistes lyriques et dramatiques ;

sages-femmes et garde-malades ;

sportifs pour la seule pratique d’un sport ;

activités de presse, etc...

Exonération de CFE en raison de la zone géographique

Certaines zones géographiques donnent lieu à une exonération de CFE. Il s'agit notamment des zones d'implantation suivantes :

les zones d'aide à finalité régionale (ZAFR) ;

les zones d'aide à l'investissement des petites et moyennes entreprises (ZAI) ;

les zones France ruralités revitalisation (ZFRR) ;

les quartiers prioritaires de la politique de la ville (QPPV) ;

les zones de restructuration de la défense (ZRD) ;

La première année d'activité, un formulaire de déclaration initiale de CFE(formulaire 1447-C-SD) doit être transmis à l'administration fiscale avant le 1er janvierde l'année suivant la création de l'entreprise. Ainsi, si vous créez une entreprise en 2025, vous devrez effectuer votre déclaration CFE avant le 1er janvier 2026.

Ce formulaire comporte plusieurs cadres :

l’identification de l’entreprise ;

l’activité professionnelle exercée de son domicile ou en clientèle ;

l’origine de l’établissement ;

l'identification de l’ancien exploitant ;

les renseignements pour l’ensemble de l’entreprise ;

les renseignements pour l’établissement ;

les biens du nouvel établissement passibles d'une taxe foncière ;

les principales exonérations.

Toutes ces informations ne doivent pas forcément être complétées : elles varient surtout en fonction de votre situation.

Autrement, les entreprises soumises à la CFE ne sont pas tenues de déclarer chaque année leurs bases d'imposition.

En revanche, une déclaration modificative 1447-M-SD doit être remplie par l'entreprise qui se trouve dans l'une des situations suivantes :

l'entreprise demande une exonération : aménagement du territoire, entreprises de spectacles vivants ou jeune entreprise innovante (JEI) ;

l'entreprise souhaite signaler une modification d'éléments connus de l'administration, tels que :

augmentation ou diminution de la surface des locaux ;

variation du nombre de salariés ;

dépassement du seuil de 100 000 € de chiffre d'affaires (pour les activités immobilières de location d'immeubles nus) ;

cessation ou fermeture d'un établissement.

Pour déclarer un changement, l'entreprise doit déposer une déclaration modificative 1447-M-SD au service des impôts des entreprises (SIE) dont elle dépend, avant le 2ème jour ouvré suivant le 1er mai (jusqu'au 3 mai 2025 pour la CFE 2026).

L'entreprise redevable de la CFE reçoit un avis d'imposition dématérialisé sur son espace professionnel impôts.gouv. Cet avis indique le montant de la CFE ainsi que le délai pour la payer.

soit en une seule fois si le montant de la CFE est inférieur ou égal à 3 000 € ;

soit en deux fois si le montant de la CFE est supérieur à 3 000 € : un premier acompte de 50 % doit être versé au plus tard le 16 juin 2025, et le solde restant doit être réglé au plus tard le 15 décembre 2025.

L'entreprise peut choisir parmi les modes de paiement suivants :

paiement en ligne (téléréglement) : mode de paiement par défaut, l'entreprise effectue elle-même le paiement de la cotisation en ligne ;

prélèvement mensuel : mode de paiement optionnel, l'entreprise est prélevée automatiquement le 15 de chaque mois, de janvier à octobre (option possible jusqu'au 15 juin) ;

prélèvement à l'échéance : mode de paiement optionnel, l'entreprise est prélevée automatiquement à la date d'échéance (option possible jusqu'au 31 mai pour l'acompte et jusqu'au 30 novembre pour le solde restant à régler).

Written by our expert Editorial staff

July 4, 2023

What is the difference between CFE, CVAE, TF and TP?

These taxes can have a negative impact on a company's cash flow. Find out how they work, so you can put the right strategy in place.

1. The basics of TF

Like the CFE, the TF (Taxe Foncière) is based on the surface area of land owned by the company. The amount of the tax varies according to the type of land and the commune.

2. CFE bases

The CFE is based on a company's surface area. The amount of this tax may therefore vary according to the location and size of the premises occupied by the company. It can also be influenced by the decision to transfer or expand a business.

3. CVAE bases

The business value-added tax (CVAE) applies to companies with sales in excess of 250,000 euros. The amount of the CVAE may therefore be influenced by whether or not the company manages raw materials, and by the way it operates, which may have an impact on its added value.

4. TP basics

TP (Taxe Professionnelle) was always deferred for two years. It was based on the company's operating surface area, plus 16% of the gross value of its real estate holdings. The Taxe Professionnelle has been replaced by the CET, which appears to be less onerous fiscally.

Il n'est généralement pas possible d'éviter de payer la CFE, car il s'agit d'un impôt local dû par toutes les entreprises exerçant une activité professionnelle non-salariée. Toutefois, il est possible d'être exonéré du paiement de la CFE si l'entreprise relève d'un des cas d'exonération.

Qui est exonéré de CFE ?

Certaines entreprises sont exonérées du paiement de la CFE : les entreprises nouvellement créées au titre de leur première année d'activité, les entreprises réalisant un chiffre d'affaires inférieur à 5 000 €, certaines entreprises en raison de l'activité qu'elles exercent et les entreprises implantées dans certaines zones géographiques.

How is the CFE calculated?

Lorsque l'entreprise dispose d'un local pour exercer son activité, la CFE est calculée en fonction de la valeur locative des biens immobiliers soumis à la taxe foncière et utilisés par l'entreprise pour son activité professionnelle au cours de l'avant-dernière année (année N-2). En revanche, si l'entrepreneur ne dispose d'aucun local et exerce son activité à domicile, le montant de la CFE est calculé en fonction d'une cotisation minimum, qui dépend du chiffre d'affaires réalisé au cours de l'année N-2 et du taux d'imposition voté dans la commune.

Are autoentrepreneurs concerned by the CFE?

Yes, like all other business creators, autoentrepreneurs are obliged to pay CFE. The rate of this local tax is calculated on the basis of the rental value of the assets used by the company.

How do I pay the CFE?

Payment of the Cotisation Foncière des Entreprises is made online at www.impots.gouv.fr. Click on the "pay" tab above the dematerialized CFE notice, once you have declared your bank account information in the professional space.

How do I declare my CFE?

The CFE declaration must be made before January 1st of the year following the company's creation.