By definition, the SAS legal form or société par actions simplifiée (simplified joint-stock company) is a commercial company made up ofat least two partners. This legal form is particularly appreciated for its operational flexibility.

Characteristics of an SAS

Created by the law of January 3, 1994, the SAS is a société par actions (joint-stock company) with fewer operating conditions than the société anonyme (public limited company).

It has several features:

- it must have at least two associates;

- the wording of the articles of association is free, not governed by law;

- the share capital is divided into shares ;

- the amount of share capital is freely determined by the partners (minimum symbolic €1);

- partners are only liable up to the amount of their contributions to the company;

- the beneficiaries of the shares making up the share capital are shareholders ;

- It must be headed by a single Chairman, who may be assisted by one or more Managing Directors.

Differences between a SAS and a SASU

In principle, a SASU, or société par actions simplifiée unipersonnelle, follows the same rules as an SAS. It is the single-member form of the SAS, i.e. it has only one shareholder. The only difference is the number of associates.

Otherwise, these two legal forms have many points in common:

- operating flexibility ;

- limited liability of partners / sole partner ;

- choice of tax regime (corporate or personal income tax) ;

- social protection for managers ;

- possibility of appointing one or more managing directors.

If you want to set up on your own, a SASU (simplified joint-stock company) can be particularly interesting, as you benefit from the same advantages as an SAS.

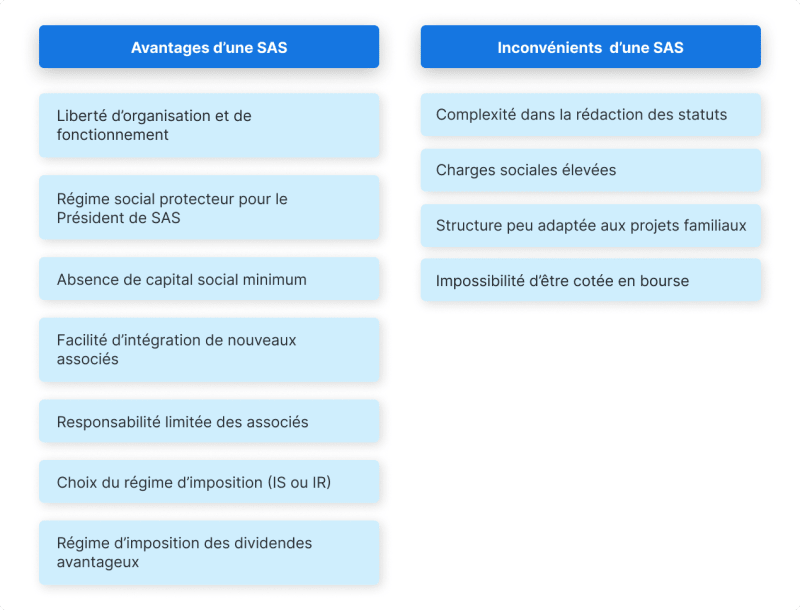

The SAS has many advantages:

- great operating flexibility;

- a protective social regime for the Chairman of SAS ;

- ease of integrating new associates ;

- limited liability of associates ;

- a choice of tax regime (corporate or personal income tax);

- an advantageous dividend tax regime.

Freedom of organization and operation

The SAS is particularly appreciated for its operational flexibility. In fact, legislation does little to regulate the operation of SASs, leaving the partners a great deal of freedom when it comes to drafting the articles of association.

The partners are free to organize the company as they see fit. This gives them considerable flexibility in defining the rules governing the organization and operation of the company. The only legal requirement is the appointment of an SAS Chairman, who will act as the company's legal representative.

When drafting the Articles of Association, the partners are free to set the decision-making procedures within the SAS, whether in terms of decision-making methods (written consultation, meeting) or voting rules (quorum, majority).

You should also be aware that some decisions can only be taken by the managing director, while others must be taken by all the associates (for example, an increase in share capital).

A major advantage of this legal form is the great freedom of organization and operation enjoyed by the associates of the SAS. Business founders can organize their company as they see fit, provided they comply with the provisions of the law.

Social security protection for the Chairman of a simplified joint stock company

The Chairman of an SAS is an "assimilé-salarié", meaning that he or she is covered by the general social security system. They benefit from the same advantageous social security coverage as conventional employees, with the exception of unemployment insurance. It is important to know that SAS directors do not contribute to unemployment insurance.

But how can you benefit from unemployment in SAS? If you wish, you can take out supplementary unemployment insurance. You can also combine your corporate office with an employment contract, provided you comply with the conditions for doing so. As the holder of an employment contract, you can then benefit from unemployment insurance in the same way as a regular employee.

The Chairman of a simplified joint-stock company (SAS) benefits from comprehensive social security coverage : sickness and maternity insurance, family allowances, work accident insurance, basic pension insurance, supplementary pension insurance and provident insurance.

In the absence of remuneration, no social security contributions are due.

Finally, you should know that dividends in SAS are not considered as remuneration and are therefore not subject to social security contributions. This means that if you choose to be remunerated exclusively in the form of dividends, you pay no social security contributions, but in return you benefit from no social security protection.

No minimum share capital

The creation of an SAS does not require a minimum share capital. This means that an SAS can be created with a minimum capital of €1.

The amount of share capital is therefore freely determined by the partners. It can be made up of contributions in cash (a sum of money) or in kind (goods other than money). It is even possible to make industrial contributions (skills or know-how).

Easy integration of new associates

In a SAS, it is relatively easy to bring new partners into the company. New partners can be brought into a SAS:

- or by an increase in share capital;

- or by selling shares.

One of the main advantages of the SAS is its ability to integrate new partners, without having to amend the Articles of Association. The SAS is not limited by a maximum number of partners. It can therefore take on an unlimited number of associates, provided this is permitted by the Articles of Association.

Share capital increase

In addition to the legal requirements governing increases in share capital, the integration of a new partner follows a formal procedure laid down in the company's bylaws. A share capital increase is decided by shareholders at an Extraordinary General Meeting (EGM), by a 2/3 majority.

Otherwise, associates can organize the entry and departure of new associates as they see fit.

Sale of shares

It is also possible to bring new partners into the SAS by organizing a share transfer, which consists of a partner (transferor) transferring to his buyer (transferee) the rights he holds in the company's share capital.

In principle, the transfer of SAS shares is unrestricted, without any approval procedure. However, the Articles of Association may contain specific clauses governing share transfers:

-

approval clause: this makes the sale subject to approval by the associates, so that they can validate the buyer chosen by the seller;

-

pre-emption clause: this gives one partner the right to buy back shares that another partner is planning to sell;

-

share inalienability clause: prohibits shareholders from selling their shares for a maximum period of 10 years.

Limited liability of associates

In principle, the liability of SAS partners is limited to the amount of their capital contributions. In other words, partners are only liable for debts up to the amount of their contributions to the company's capital.

In practical terms, the assets of the company and those of the partners are kept separate. As a result, the associates of an SAS cannot lose more than the amount of their initial contribution to the SAS. In the event of debts, creditors will not be able to seize assets belonging to the associates.

Only in the case of loans granted by creditors, with security taken over the partners' personal assets, can the partners' liability be extended.

Choice of tax regime (corporate or personal income tax)

The SAS benefits from an advantageous tax regime, particularly when it comes to taxing profits. You can choose between corporate income tax (IS) and income tax (IR).

By default, the profits of an SAS are subject to corporate income tax (impôt sur les sociétés - IS). However, when you set up your company, you can override this rule by opting for income tax if several conditions are met:

- The SAS must have been created less than 5 years ago;

- it must have fewer than 50 employees;

- annual sales of less than 10 million euros;

- it must not be listed on the stock exchange.

Please note, however, that the IR option is limited to 5 consecutive financial years.

Advantageous dividend tax regime

SAS shareholders may opt to receive remuneration in the form of dividends. In this case, their remuneration is not subject to social security contributions.

What's more, shareholders who receive dividends benefit from attractive tax treatment. Dividends are classified as income from movable capital and are taxed at a flat rate of 30%(12.8% income tax and 17.2% social security contributions).

They can also opt to be taxed at the income tax rate (0-45%).

Although SAS offers many advantages, you should not forget to consider its disadvantages when choosing your legal status.

SAS can have a number of disadvantages:

- the complexity of drafting bylaws;

- high payroll taxes ;

- a structure ill-suited to family projects.

Complexity in drafting bylaws

The statutory freedom of an SAS can be a double-edged sword. Drafting the articles of association can be a complex task, requiring a great deal of rigor and technical and legal expertise.

As the law provides very little guidance on the organization and operation of SAS, you need to be careful about :

- omission of one of the mandatory items in the articles of association (duration of the company, company name, corporate purpose, registered office, amount of share capital, etc.);

- the inclusion of unlawful clauses;

- theomission of clauses necessary for the proper functioning of the SAS or for a specific situation of the partners (for example: the pre-emption clause, which enables a partner to buy back, as a priority, the shares that another partner is considering selling).

In short, if you decide to set up an SAS, it's essential to draft the articles of association carefully , and not to forget anything. Omitting elements or remaining too imprecise in the drafting of the articles of association could lead to blockages in future decision-making.

It is therefore advisable to call on a legal professional to draw up the articles of association of an SAS and to obtain advice on the clauses to be put in place.

High payroll taxes

As mentioned above, SAS directors benefit from the protective regime of assimilés-salariés, similar to that of traditional salaried employees. In return, however, social security contributions are higher than those payable under the Sécurité sociale des indépendants (SSI) system.

Please note, however, that if managers are not remunerated, they do not have to pay social security contributions.

Structure ill-suited to family projects

The SAS is not well suited to family projects. Indeed, entrepreneurs who want to set up a family business prefer the SARL (limited liability company), as the SAS does not allow them to benefit from the protective status of collaborating spouse.

Please note: The status of collaborating spouse of a SARL (limited liability company) enables the spouse working in the company to benefit from social protection even if he or she is not paid.

Unable to be listed on the stock exchange

Unlike sociétés anonymes (SA), an SAS is not allowed to be listed on the stock exchange, which can be an obstacle for companies wishing to raise funds on the financial markets.

To remedy this problem, they may choose to turn to other means of financing if they wish to develop their projects. These may include private fund-raising or the use of venture capitalists.

Comparison table: advantages and disadvantages of an SAS

As mentioned above, the SAS has many advantages over other legal forms, notably the SARL. These two seemingly similar legal forms do have their differences.

Unlike the Chairman of an SAS, the manager of a SARL is considered a "travailleur non salarié" (TNS) affiliated to the Sécurité sociale des indépendants (SSI). They pay lower social security contributions, but on the other hand, their social security coverage is less advantageous than that of an SAS.

The SARL is better suited to family projects: it is even possible to create a family SARL to facilitate the transfer and management of family assets.

The choice between an SAS and a SARL therefore depends on the specifics of your project. If you're looking for flexibility in the organization and operation of your company, then an SAS may be more appropriate. If you're planning to run your business as a family, then a SARL may be preferable.

As you can see, it's important to consider the advantages and disadvantages of each legal form before making your choice.

To set up an SAS, several steps must be taken:

-

draw up the articles of association ;

-

set up and deposit the share capital with a bank: the share capital is deposited in a blocked account, and in exchange, the bank provides a certificate of deposit of the funds required for registration;

-

choose your registered office address : your SAS can be domiciled with a domiciliation company such as SeDomicilier ;

-

publish a notice of incorporation in a legal gazette (JAL) : the price of the legal announcement depends on the number of lines;

-

submit the application for registration on the Guichet unique website managed by INPI. Don't forget to enclose the required supporting documents, including a sworn statement of non-conviction and filiation, and a copy of both sides of a valid national identity card or passport.

Conclusion

The SAS is a legal form that offers a number of advantages, including great flexibility in drafting its articles of association and limited liability for its partners. It also has some disadvantages, which are important to consider before choosing this status.

Remember that the choice of legal form depends above all on the nature of your project and your development prospects.