What is a SARL?

As with any entrepreneur about to set up his or her own business, the first question that arises is: which status is best suited to the business I want to run?

It's not easy to choose between all the different legal forms available. This choice determines the rate of taxation, the fixed and variable costs the company will pay, and the responsibility of its manager.

Let's start with the definition of a SARL. The Société à Responsabilité Limitée (SARL) is a very common form of company, and one that is easy to manage on a day-to-day basis. It is a commercial company with a minimum of two partners and a maximum of one hundred. It comprises one or more managers, and is a form suited to small and medium-sized businesses.

Associates can be natural persons (minors or adults) or legal entities (an association, another company, etc.).

As the name suggests, in this type of company, liability is limited, both for the manager(s) and the partners. Liability is reduced to the amount of the contributions, i.e. the share capital paid in by each partner at the outset, which limits the risks for them. In effect, this means that the partners' business assets are separated from their personal assets, so that their personal assets are protected in the event of company debts.

Nevertheless, the managing director is responsible for the management of the company, both civilly and criminally, and for any mismanagement or losses. For example, in the event of late declaration of cessation of payments, i.e. outside the time limit, the manager may be ordered to pay part of the SARL's debts.

If the company is wound up, all the shares must be sold.

SARL share capital

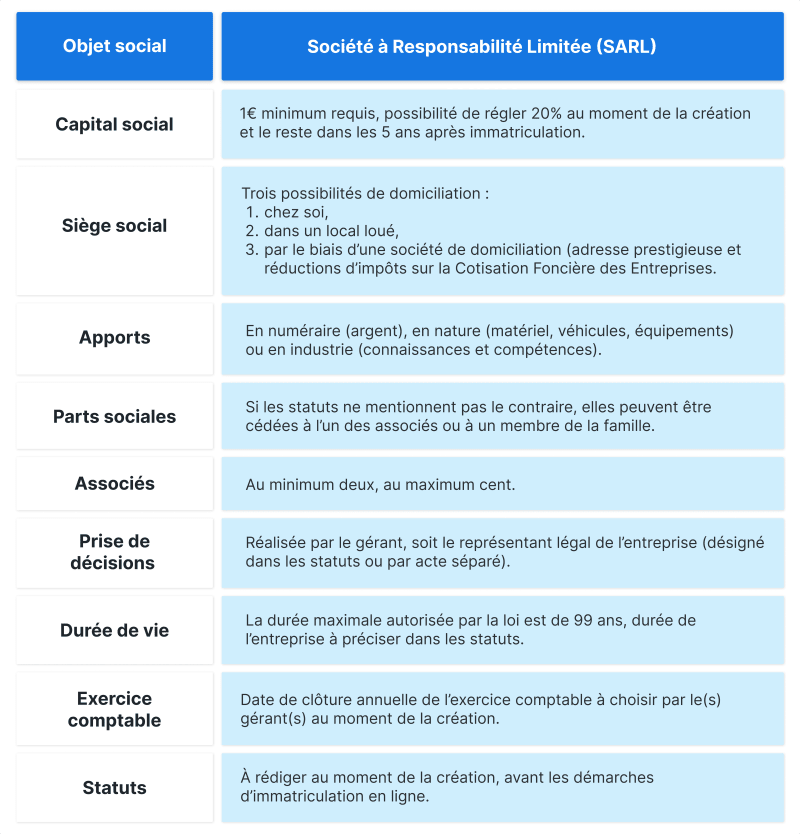

By law, there is no minimum share capital required to create a limited liability company (SARL). To become a partner, you simply need to make a contribution to the company's share capital, in return for shares.

A shareholder receives shares, and thus dividends in the form of quotas in the event of profits, but they come with rights and duties: active participation in the life of the company at Ordinary General Meetings (OGM) and Extraordinary General Meetings (EGM).

The share capital consists of :

-

cash contributions,

-

in-kind contributions (such as equipment: car, computer, etc.),

-

contributions in kind (specific know-how and skills made available).

Cash contributions must be made in a specific way: the partner pays 20% of the contributions when the SARL is created, and the balance is paid within five years of the company's registration.

Contributions in kind are just as precise: the property or object is transferred for the benefit and inventory of the company, and an auditor is required to value it. That said, the partners may revoke this obligation and not appoint an auditor if two conditions are met: no single contribution in kind exceeds 30,000 euros, and the total value of contributions in kind does not represent more than half the share capital.

Who manages a SARL?

At least a manager to administer a SARLbut there may be several. The manager must be a natural person, and may or may not be a partner in the company. The manager is appointed by the partners in the articles of association, or by separate deed at an Ordinary General Meeting (AGM).

It is the manager's duty to carry out all acts of management, i.e. everything that enables the company to function on a day-to-day basis.

To this end, the manager may :

- hire employees,

- sign contracts,

- act in legal proceedings.

The manager's decisions must be in the interest of the SARL, otherwise they may be qualified as mismanagement and engage his liability.

Each year, the manager(s) organize(s) a General Meeting with the associates to validate the accounts and the distribution of profits.

Good to know: Sometimes, the Managing Partners' powers are limited by the company's Articles of Association. In this case, they need prior authorization from the partners to perform certain acts, such as contracting loans, overdrawing current accounts, or having the company guarantee its commitments to third parties.

General Meetings of the SARL

To be able to make decisions and move forward together in the life of the company, the managing director convenes the associates to general meetings, at least two weeks before the said meeting.

Ordinary General Meetings (AGMs ) are held to :

- approve the SARL's annual financial statements,

- distribute profits,

- appoint, dismiss and determine the remuneration of the Executive Chairman.

Resolutions are passed by a majority of associates representing at least half of the shares.

Extraordinary General Meetings (EGMs ) are used to amend the articles of association of a limited liability company (SARL). There are many reasons for this: change of company name, increase in share capital, transfer of registered office, etc.

Resolutions are passed by a two-thirds majority of the shares held by the associates present or represented, or by a three-quarters majority if the company was created before August 4, 2005.

The SARL tax system

From a tax point of view, the taxation system is different for the partners and the manager of an SARL.

The SARL is subject to corporate income tax (impôt sur les sociétés - IS), but in certain cases, the company can benefit from personal income tax (impôt sur les revenus des personnes physiques - IRPP), similar to the income tax (Impôt sur le revenu - IR). The SARL must be less than five years old, or be a family company, and the partners must be unanimous.

Characteristics of the SARL

What better way to sum up all the elements we've just seen that characterize the operation of an SARL than with a summary table?

Now that you're familiar with this legal form, let's get down to business! There are a number of administrative formalities involved in setting up an SARL. To give you the best chance of success, we've put together a step-by-step guide to help you complete each formality.

Choosing your head office: company domiciliation

Le company's registered office must be specified when the company is set up. This is a central issue, as the address determines the company's nationality, its country of taxation, and the competent legal authorities in the event of a dispute. That's why it's the first thing you need to decide before you can begin the administrative formalities.

The entrepreneur has three possible choices. He can :

- register your SARL at your personal address,

- lease commercial premises,

- use a domiciliation company.

This last option enables the company to take advantage of a prestigious address , giving it a high profile with its partners, an administrative secretariat, legal assistance and meeting rooms. Our à la carte services are designed to suit all budgets.

Above all, it allows the entrepreneur to concentrate on high value-added tasks.

Last but not least, a company domiciliation protects the privacy of its manager, who will not need to disclose his or her personal address.

Appointing the SARL's manager

Before actually setting up the company, the partners involved in creating an SARL must also appoint a manager, by drawing up a deed of appointment.

You also have the option of appointing the managing director by mentioning his or her name directly in the company's articles of association. Drafting the articles of association is the next stage in the process of creating an SARL.

However, this solution will later require you to file a new version of the articles of association with the commercial court clerk's office in the event of a change of manager, at a cost of €500.

Estimate the SARL's share capital

The share capital is therefore composed, as we have seen above :

- contributions in kind designated in the bylaws (equipment, vehicles),

- industrial contributions (skills and know-how),

- cash contributions, i.e. money.

Cash contributions

Once the articles of association have been drawn up and signed, the associates must make a cash contribution to the company. They must be deposited in a blocked business account with a bank, notary or Caisse des Dépôts. A certificate of deposit will be issued and must be attached to the registration file.

If the managing director chooses to deposit the cash contributions of the share capital in a blocked bank account, he or she must create a professional bank account for the SARL (with the physical or online bank of his or her choice, some of which are free), so that each partner can deposit the various sums making up the cash contribution, which will be blocked until theKbis extract is presented.

There is no minimum amount for cash contributions to the share capital, as long as 20% of the contributions are paid when the SARL is created, and the balance paid within five years of the company's effective registration.

Contributions in kind

The contributions in kind are contributions of movable or immovable property. It is not necessary to appoint a commissaire aux apports if the value of an asset does not exceed €30,000, or if the total value of the contributions does not exceed half the company's share capital. All associates must agree to the appointment of the commissaire aux apports.

Drafting and filing the articles of association of the SARL

The registered office is decided, the manager appointed, the share capital assessed: that's it, we're off to the start-up! Let's start at the beginning: we need to draw up the articles of association for the SARL, by notarial deed.

Drafting and filing the articles of association is an important stage in the creation of your SARL. The articles of association make it possible to :

- define the SARL's operating rules,

- to govern the relationship between the company's partners,

- record the amount and payment of share capital by each associate.

For this somewhat technical stage, don't hesitate to ask your notary, or even a lawyer or solicitor, to help you decide what's best for you.

By law, the articles of association must include the following information:

- the company's legal form,

- company name,

- head office address,

- corporate purpose,

- the duration of the company (up to 99 years),

- the amount of share capital to be paid in cash,

- the identity of the appointed manager (unless he or she is appointed at a later date by a formal appointment at an EGM),

- the identity of the founding partners for cash contributions and proof that the funds have been deposited with your bank,

- the terms and conditions for paying up cash contributions,

- the valuation of any contributions in kind,

- in the case of industrial contributions, the terms and conditions for subscribing to shares through industrial contributions,

- the distribution of shares among associates,

- and operating procedures.

Next, all the founding partners of the SARL must sign the articles of association, and the manager must date and certify them. It is also advisable to draw up a pact uniting the partners, to make the articles of association more flexible. They can be drawn up by notarial deed or private deed, and registered with the clerk's office of the relevant commercial court within one month of signature.

Create a business bank account

Company founders are required by law to have a business account dedicated to the company (for income and expenses).

Creating your business bank account can be set up directly with any physical or online banking institution, according to the terms and conditions defined with your financial advisor. This account will be used first and foremost to deposit cash contributions towards the company's share capital.

Paying in the SARL's share capital

Before applying for registration of the SARL, you must deposit the funds corresponding to the company's share capital in the business bank account you have set up.

Each partner pays an amount into this account according to what has been defined in the company's articles of association. As mentioned above, 20% of contributions are paid when the SARL is created, and the balance is paid within five years of the company's effective registration.

The business account into which the share capital is paid is blocked until the Kbis extract proving the company's registration is presented.

Publish a notice in a Journal d'Annonces Légal (JAL)

Publication of the company's incorporation notice in a legal gazette (JAL) is necessary for the final step: applying for company registration. You'll need the publication notice to complete your company registration form.

You can request publication in a legal gazette (JAL) or online press service (SPEL) authorized in the département where the SARL's registered office is located. Use the interactive map on the government website to find out which media are authorized to publish legal notices (SHAL).

The SARL incorporation notice must contain the following information:

- The company's creation date,

- Company name and acronym,

- Its legal status (SARL),

- Total amount of share capital,

- head office address,

- Corporate purpose,

- the duration of the company,

- Surnames, first names and contact details of managers and associates with decision-making authority and authority to bind the company to third parties;

- The company's registry office.

Publication costs vary, but in 2025 they will be around €147 in mainland France and €171 for Mayotte and Reunion.

Create your SARL online

To set up a Limited Liability Company (SARL), here are the essential steps to follow, taking into account the legal requirements in force.

Setting up an online business means applying to register your company online, to validate and formalize its existence on the business market, and legitimize its rights and obligations.

Since January 1, 2023, it has been mandatory for all entrepreneurs to use the " guichet unique des entreprises"for business start-up, modification and closure formalities.

You will therefore be able to apply for registration via this electronic one-stop shop, by filling in a form and submitting the required supporting documents:

- the completed M0 form,

- signed articles of association,

- certificate of deposit of share capital,

- certificate of publication of the notice of incorporation,

- a declaration of beneficial owners,

- documents relating to the manager (ID, sworn statement of non-conviction, filiation certificate).

Once these formalities have been completed, and the file has been validated by the Registrar, the SARL will be registered with the Registre du Commerce et des Sociétés (RCS), giving it legal personality and enabling you to start trading.

It is advisable to consult a legal professional or chartered accountant to help you with these steps, and to ensure that they comply with current legal requirements.

You've reached the end of the long formalities. Congratulations, your limited liability company has been created!