Opting for a non-trading property company (SCI) tax-exempt can help optimize costs, but also entails specific tax constraints. Why choose a non-trading property company subject to corporation tax? What are its advantages and disadvantages? This article guides you through the essential points you need to know before making your choice, and helps you understand whether this tax regime is right for your real estate project.

👉 The first essential step is to choose your domiciliation of your SCIan administrative obligation that determines its legal and tax address. We explain!

Understanding SCI and its tax options

The Société Civile Immobilière (SCI) is a legal structure for acquiring, managing and transferring real estate assets. It offers a degree of flexibility in terms of organization and the distribution of shares among associates.

Unlike commercial companies, an SCI may not carry out an industrial or commercial activity on a principal basis, which excludes, in particular, professional furnished rental.

Possible tax regimes for an SCI

An SCI can be subject to two different tax systems:

-

Income tax (IR). This is the default system. Each partner is taxed on his or her share of profits, according to his or her own tax rate. This system is often preferred for long-term investments, as it gives access to the often more advantageous capital gains tax system for private individuals.

-

Corporation tax (IS). An SCI can opt for corporate income tax at the time of its creation or during its lifetime. In this case, it becomes an independent tax entity, taxed directly on its profits. This option allows the property to be depreciated and certain expenses to be deducted.

Why opt for a non-trading property company subject to corporation tax?

Opting for the corporation tax regime can be a good way of optimizing the taxation of a real estate project, notably by reducing the tax base through tax deductions. However, it also entails stricter accounting obligations and potentially heavier taxation in the event of property disposal.

Before making a choice, it's essential to assess the long-term profitability and tax impact.

Advantages of SCI tax status

There are several advantages to opting forcorporate income tax (CIT) for real estate investors. In particular, it offers greater tax control, optimized expenses and easier management of profits. Here are the main advantages.

Property depreciation

One of the main advantages of SCI à l'IS is its ability to depreciate the property. Unlike an SCI subject toincome tax (IR), where deductible expenses are limited, an SCI subject to corporate income tax can record depreciation of the property as an expense.

This means that each year, a portion of the property's value is deducted from taxable income, thereby reducing the corporation tax payable by the SCI.

For example, a €500,000 asset depreciated over 30 years at a rate of 3% per year would allow €15,000 to be deducted from taxable profit each year.

Deduction of charges and expenses

In addition to depreciation, an SCI subject to corporation tax can deduct a number of expenses from its taxable income:

-

Notary fees related to the acquisition of the property,

-

Maintenance and renovation work,

-

Management costs, including accounting fees and any remuneration paid to the manager,

-

Financial expenses, such as interest on loans.

These deductions reduce the tax payable and optimize the profitability of the investment.

Controlling taxation of associates

In a SCI that paysincome tax (IR), each partner is taxed on his or her share of the profits, whether or not he or she receives them. On the other hand, a non-trading property company subject tocorporation tax (impôt sur les sociétés - IS) pays corporateincome tax, and associates are taxed only when dividends are distributed. This makes for better tax management for the partners, who can choose when and how many dividends to receive, in order to optimize their own taxation.

Profit transfer and capitalization

A non-trading property company (SCI) subject to corporation tax can capitalize and reinvest its profits without the partners having to pay tax on property income.

This strategy is particularly interesting for those wishing to build up a real estate portfolio over the long term by reinvesting profits directly in the acquisition of new properties.

What's more, as part of an asset transfer,corporate income tax can help optimize tax liability, notably by limiting inheritance tax on SCI shares.

Opting for thecorporate income tax system enables investors to reduce their tax base, better manage the taxation of associates and reinvest profits more easily. However, this strategy also has its drawbacks, particularly in terms of capital gains tax, which we will discuss in the next section.

Disadvantages of non-trading property companies (SCI à l'IS)

Whilecorporation tax (impôt sur les sociétés - IS) offers a number of advantages for an SCI, it also has some significant disadvantages. Before opting for this tax system, it's important to understand its limitations, so you can assess whether it's right for your real estate investment strategy.

High capital gains tax on real estate

One of the main disadvantages of the SCI à l'IS is the way capital gains are taxed. Unlike a property investment company subject to income tax, where capital gains are progressively deducted according to the length of ownership (up to total exemption after 30 years), a non-trading property investment company subject to corporation tax does not benefit from any deduction.

The capital gain is calculated on the basis of the net book value, i.e. the value of the asset after deduction of depreciation booked over the years. The result: the more depreciation has reduced the value of the asset, the higher the taxable capital gain on resale.

Example: An asset purchased for €500,000 and depreciated over 30 years at a rate of 3% per annum sees its book value fall to €350,000 after 10 years. If the property is resold for €600,000, the taxable capital gain will be €250,000 (€600,000 - €350,000) instead of €100,000 in a SCI subject to income tax.

Onerous accounting obligations and high management costs

Unlike an SCI subject to income tax (IR), where accounting is simpler, an SCI subject to corporation tax (IS) must :

- Complete commercial accounting (balance sheet, income statement, accounting appendices).

- File your annual financial statements with the Greffe du Tribunal de Commerce.

- Submit specific tax returns (form 2065 for corporate income tax, 2033 for the income statement).

These obligations often require the involvement of a chartered accountant, which generates additional costs estimated at between €1,500 and €3,000 per year.

Double taxation of profits

In an SCI subject to corporation tax, profits are taxed in two stages:

-

Corporation tax (15% on the first €42,500 of profits, then 25% thereafter).

-

Taxation of dividends received by associates (single flat-rate withholding tax of 30%, or progressive personal income tax scale).

This double taxation can significantly reduce partners' earnings compared with a SCI subject to income tax, where rents received are taxed directly according to each partner's share.

Fewer tax breaks for passing on wealth

The transfer of shares in a non-trading property company (SCI) subject to personal income tax (IR) is more advantageous from a tax point of view, thanks to deductions on gift and inheritance tax. For SCIs subject to corporate income tax, these advantages are less attractive, which can be an obstacle for those wishing to optimize the transfer of their real estate assets to their heirs.

While opting forcorporate income tax allows for better tax management in the short term, it entails heavier accounting and tax constraints. The high taxation of real estate capital gains, management costs and double taxation of profits are all factors to be taken into account before making this choice.

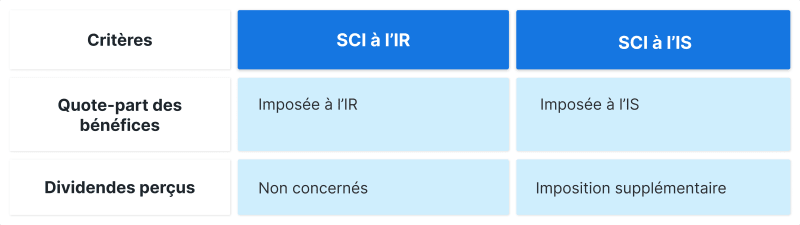

SCI à l'IR vs SCI à l'IS comparison

The choice between an SCI subject to income tax (IR) and an SCI subject to corporation tax (IS) depends on a number of criteria: the length of time the assets are held, the profitability sought, and the partners' tax situation. Here's a comparison of the two systems.

Income tax: IR vs. IS

In a SCI subject to income tax, associates are taxed directly on their share of profits. Conversely, a non-trading property company (SCI) subject to corporation tax (IS) allows the assets to be depreciated and more expenses to be deducted, but the profits are first subject to corporation tax before being redistributed to the partners in the form of dividends, resulting in double taxation.

Managing real estate capital gains

Capital gains tax is a key criterion. In a SCI subject to income tax, capital gains are taxed according to the system applicable to private individuals, with a progressive allowance (total exemption after 30 years). In a SCI taxable under the IS system, capital gains are calculated on the basis of net book value, which often results in higher taxation.

Taxation of associates

In a SCI subject to income tax, profits are taxed immediately, whether or not they are redistributed. In a SCI taxable under the IS system, taxation only takes place when dividends are received, offering greater flexibility.

-

SCI à l'IR: Advantageous for long-term investors, simpler to manage, but less flexible fiscally.

-

SCI à l'IS: Interesting for short-term tax optimization, but with high capital gains tax and strict accounting obligations.

When should you choose an SCI tax-exempt company?

The choice between an SCI subject to income tax (IR) and an SCI subject to corporation tax (IS) depends on the partners' objectives, the way the assets are managed and the long-term wealth strategy. Here are the cases in which opting forcorporation tax may be advantageous.

👉 Before opting for this tax system, it's essential to assess your reasons for doing so. create an SCIas each structure offers specific advantages depending on your real estate project.

For investors seeking short-term tax optimization

One of the main advantages of SCI à l'IS is the possibility of depreciating the property and deducting numerous expenses. This system is particularly interesting for investors wishing to reduce their tax base and maximize deductible expenses (notary fees, loan interest, maintenance, manager's remuneration).

Example: An investor owning several rental properties through a non-trading property company (SCI) can optimize his tax situation by reinvesting profits in new purchases, without being immediately taxed on these gains.

For those who want to master the taxation of associates

In a SCI subject to income tax, partners are taxed on the company's profits, whether they receive income or not. Conversely, a non-trading property company (SCI) subject to corporation tax (IS) lets you choose when to distribute dividends, offering better individual tax management.

This mode of operation is attractive for associates with variable income or those wishing to smooth out their tax burden over several years by delaying the collection of dividends.

For furnished rental projects

An SCI (non-trading property company) subject to corporate income tax cannot be used to carry out a commercial activity such as furnished rental, which is considered to be a commercial activity.

On the other hand, a non-trading property company (SCI) subject to corporation tax (IS) can legally carry out this activity, enabling it to operate properties under LMNP (Loueur Meublé Non Professionnel) status, while retaining the advantages of a non-trading company.

For those wishing to reinvest their profits

In a non-trading property company subject to corporation tax, profits can be retained within the company for reinvestment in new real estate projects. This allows property assets to grow more rapidly, without the partners having to pay immediate tax on their profits.

Opting forcorporate income tax is a strategic choice for investors wishing to reduce immediate taxation, reinvest profits and manage dividend distribution more closely. However, it is important to anticipate the tax consequences for the resale of assets and the transfer of assets.

Accounting and administrative obligations of an SCI subject to corporate income tax

Opting for an SCI subject to corporate income tax (impôt sur les sociétés - IS) entails more onerous accounting and administrative obligations than for an SCI subject to personal income tax (impôt fiscal - IR). These constraints must be taken into account before making a tax choice.

Rigorous bookkeeping

Unlike an SCI subject to income tax (IR), which benefits from simplified accounting management, an SCI subject to corporation tax (IS) is subject to the same obligations as a commercial company. It must :

-

Complete bookkeeping with balance sheet, income statement and accounting appendices,

-

Record all financial transactions (purchases, sales, expenses, depreciation),

-

Draw up an accurate annual income statement and balance sheet.

The services of a chartered accountant are often recommended, at an annual cost of between €1,500 and €3,000.

Filing of annual financial statements

Every year, a SCI (non-trading property company) subject to corporation tax must file its financial statements with the Registrar of the Commercial Court (Greffe du Tribunal de Commerce). While this requirement ensures financial transparency, it also entails an additional administrative burden.

Specific tax returns

In addition to accounting management, an SCI subject to corporate income tax must :

- Declare profits using form 2065 (income tax return for companies subject to corporation tax),

- Complete financial and tax statements (Form 2033 for small businesses),

- Calculate and paycorporate income tax (15% up to €42,500 profit, then 25% above).

In a nutshell

Whilecorporate income tax allows you to optimize your tax situation, it also imposes more complex accounting and administrative formalities. These obligations must be anticipated before opting for this system.

Steps to set up an SCI tax-exempt company

Setting up a non-trading property company (SCI) subject to corporation tax (IS) follows the same steps as for a conventional non-trading property company (SCI), with a few specific features linked to the choice of tax regime. Here are the steps to follow.

Drafting the SCI's articles of association

The Articles of Association define how the company operates and the rights and obligations of the partners. They must include a number of compulsory clauses:

- Company name,

- Corporate purpose (property management),

- Share capital (fixed or variable),

- Decision-making procedures,

- Distribution of shares among associates.

For SCIs subject to corporate income tax, it is advisable to state explicitly in the bylaws that the company has opted for this tax regime.

👉 To simplify these procedures, many entrepreneurs choose to create their SCI onlineto save time and avoid administrative errors.

Registering the SCI and obtaining its registration

Once the articles of association have been drawn up and signed, the SCI must be registered with the Registre du Commerce et des Sociétés (RCS). This involves :

- Publication of a notice of incorporation in a legal gazette,

- The registration file with the Registry of the Commercial Courtincluding :

- Bylaws signed,

- The completed M0 form,

- A declaration of beneficial ownership,

- Proof of registered office address.

Once these formalities have been completed, the SCI obtains a Kbis and a SIREN number.

Opting for corporation tax

By default, an SCI is subject toincome tax. To be taxed under the corporation tax (IS) regime, it must apply to the corporate tax department (Service des Impôts des Entreprises - SIE) within 3 months of registration. This option is irreversible.

Setting up a non-trading property company (SCI) subject to corporation tax requires careful preparation, particularly when it comes to drafting the articles of association and choosing thetax option. Once registered, you must comply with accounting and reporting obligations to avoid any tax adjustments.

Conclusion

The choice between a SCI subject to income tax and a SCI subject to corporation tax is based on an in-depth analysis of the partners' financial and tax objectives. Whilecorporate income tax allows better optimization of expenses and more flexible management of profits, it also imposes heavier accounting and tax constraints, particularly in terms of capital gains on real estate.

Before opting for this system, it is essential to assess its long-term impact. To simplify the creation and management of your non-trading property company (SCI), SeDomicilier offers tailored solutions to facilitate your administrative and tax procedures.